Getting started: download, signup, and the moment of truth

Most people who try a new financial app want two things: speed and clarity. The user journey begins the instant you tap install — that first screen matters. For many riders and gig workers in Ciudad de México, the flow from download to approval is what decides if they stick. When you open the app and go through digital onboarding, expect a quick KYC step, a soft credit check for your initial credit limit, and an interface that shows the card offer clearly. If you want to compare offers fast, chécalo aquí: didi prestamos.

Activation to first transaction: the practical steps

Once your mi tarjeta de crédito appears in the app, activation usually takes minutes. Link a bank account, set a PIN, and choose whether to enable contactless payments. The app often displays APR and expected fees up front — no guesswork. Use the first small charge to verify a merchant and to check alerts: push notifications should tell you available balance and pending authorizations. This is when the credit score impact is minimal if you keep utilization low and pay on time.

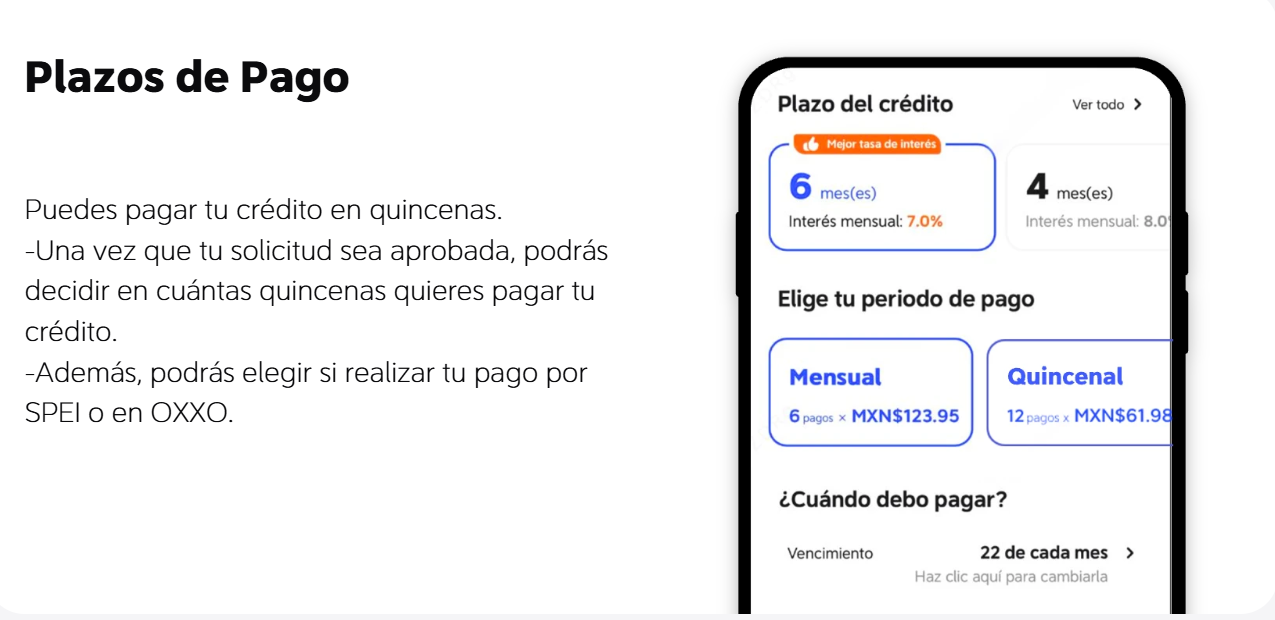

Daily use and maintenance: what you’ll actually do

Day-to-day, the app should help you manage purchases, view statements, and set up autopay. Look for features like spending categories and minimum payment reminders. If you accept instant loans or short-term advances, the process labeled prestamos en linea al instante needs clear repayment terms so you don’t pay unnecessary interest. Track your interest rate and due dates — a small habit that avoids surprises.

Common mistakes users make — and how to dodge them

People skip reading the fine print or they treat the card like free money. That bites back when APR compounds or when cash advances incur steep fees. Another misstep is ignoring alerts — autorizar a un gasto pequeño confirms the merchant works; ignoring it can hide fraud. Also, mixing multiple small loans without syncing due dates creates overdraft risk. A quick habit: reconcile purchases weekly. It takes ten minutes and saves headaches — trust me, it makes a difference.

How DiDi Finanzas fits a user’s life

DiDi Finanzas designs the cycle to match gig rhythms: fast approvals, in-app controls, clear statements and integration with ride/delivery earnings. For folks whose day is split between blocks of deliveries and home time, that clarity is priceless. The platform leans on simple credit terms, so you can see how charges affect your credit limit and plan repayments. Real-world anchor: drivers in Mexico City often rely on predictable cash flow patterns — a predictable credit tool helps stabilize that cash flow during low-demand days.

Alternatives and quick comparisons

Other players may offer lower APR or bigger limits, but they might require longer underwriting or more paperwork. Some fintechs emphasize rewards, which is great if you spend on specific categories. Compare on three axes: approval speed, transparency of fees, and account controls. If speed and simple repayment matter more than points, then a product built for gig workers tends to win.

Golden rules for choosing and using a credit tool

1) Confirm total cost: compare APR and all fees, not just the headline rate. 2) Match billing cycles to income: align due dates with pay days to avoid missed payments. 3) Use credit limits as cushions, not budgets — stay well under the limit to protect your credit score and avoid interest spikes. These three metrics keep things sane and actionable.

Closing note

Good tools reduce noise and give you control — that’s when they matter. After walking through setup, first use, everyday management, and common traps, the practical takeaway is clear: choose a service that shows fees, supports fast onboarding, and fits your rhythm. For many usuarios, that combination is precisely what DiDi Finanzas brings to the table — simple, tuned to gig life, and built to move with you. —